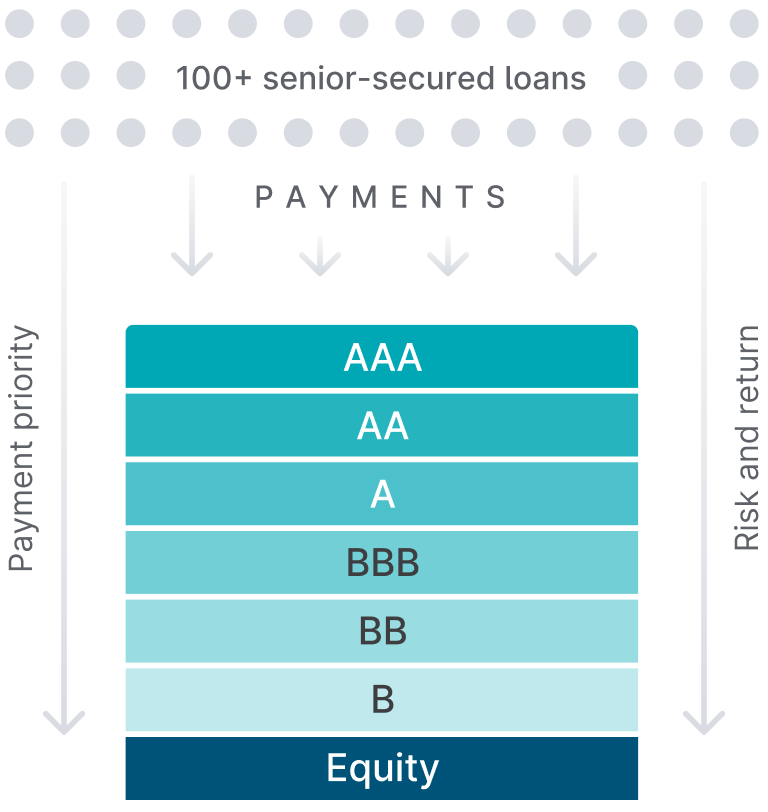

Senior-secured loans pooled into a CLO

Asset managers typically purchase 200+ senior-secured corporate loans to form a CLO.

Investors allocate to tranches

To fund the purchase of the loans, the manager sells stakes in its CLO to debt and equity investors.

The debt portion of the CLO is organized into multiple levels, known as tranches, that investors can select from. A final equity tranche sits at the bottom.

Earn quarterly income

As loans in the CLO distribute principal and interest, cash flows from the top tranche down on a quarterly basis.

Not until all interest owed to the AAA tranche is paid does AA receive payments, and so on.

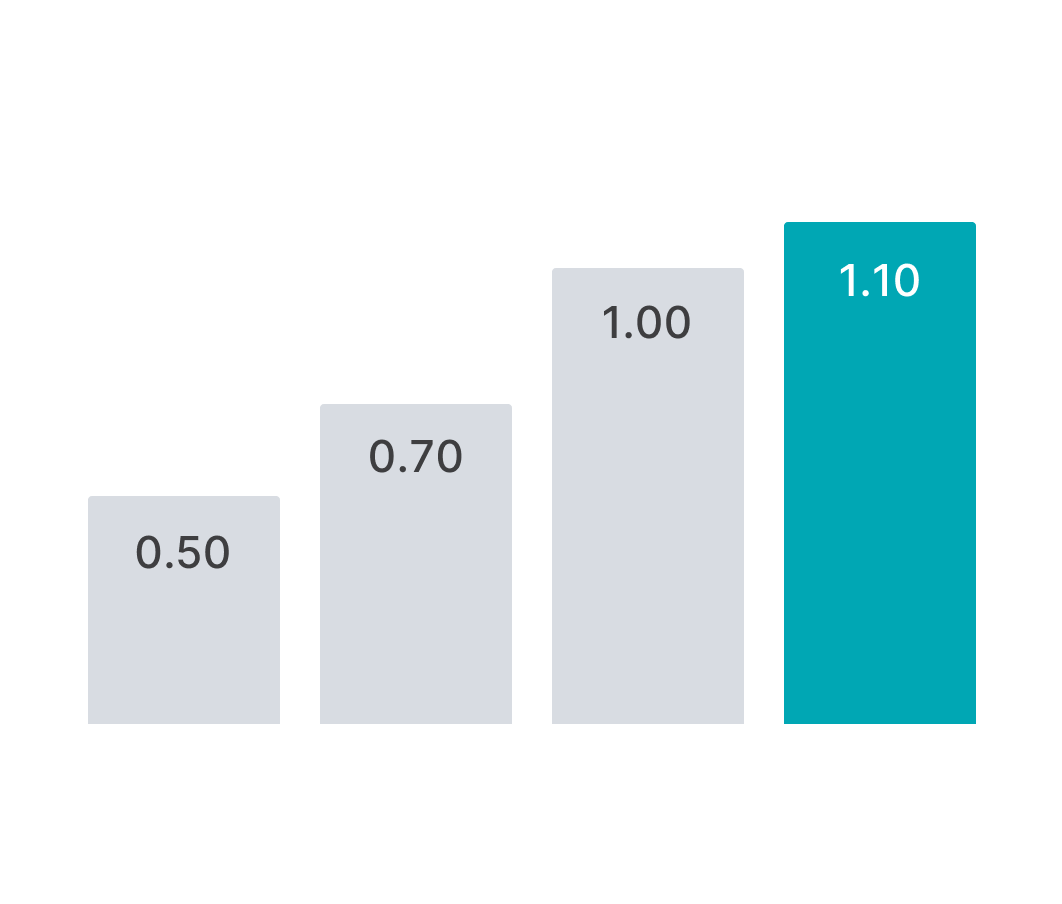

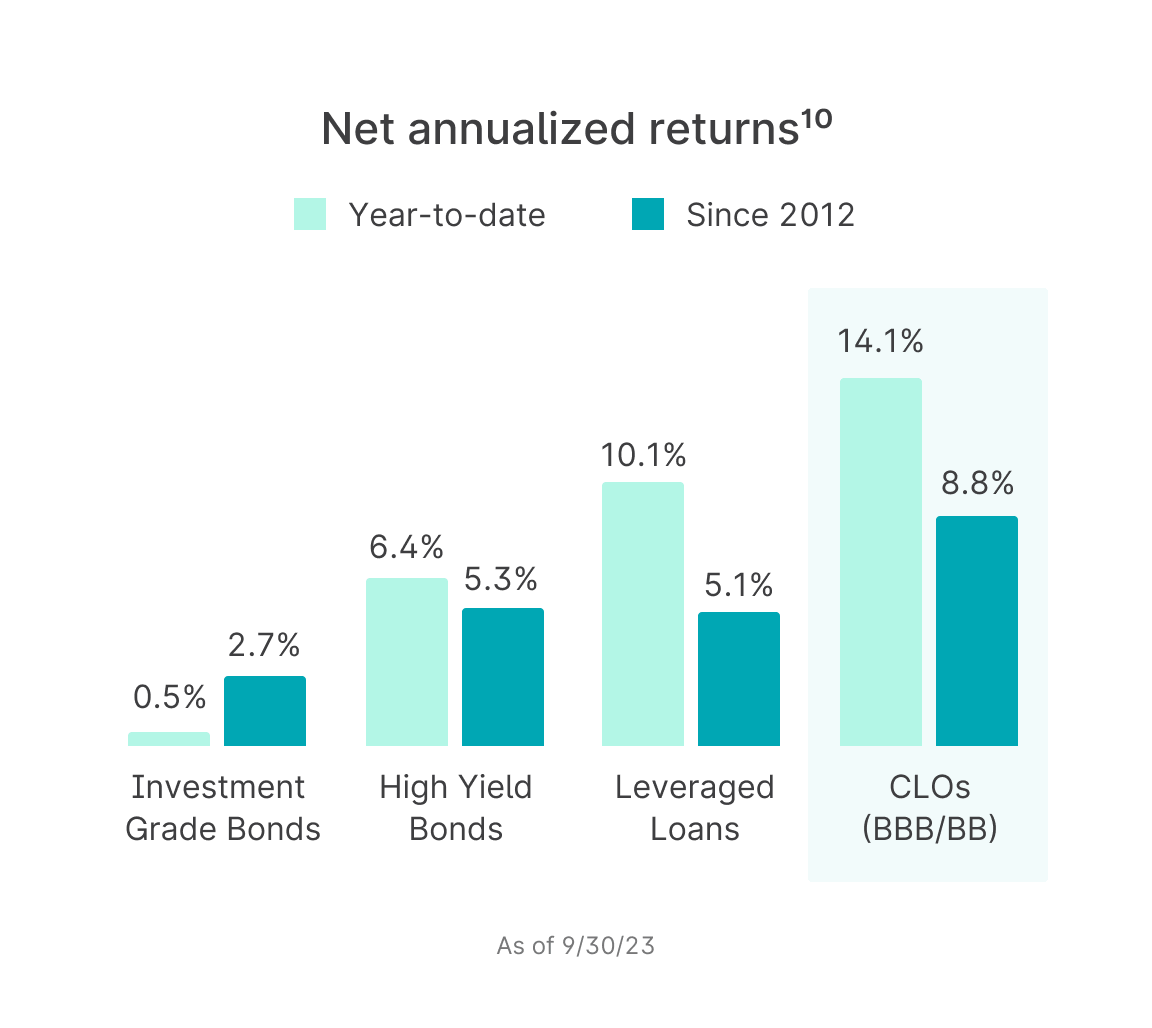

Delivering competitive historical returns with reduced risk

We believe the BBB and BB tranches of CLOs have the opportunity to deliver some of the most attractive risk-adjusted returns in fixed income.

Outperform traditional fixed income

The BBB and BB tranches that our Funds target historically offer higher yields than similarly rated corporate bonds and other structured products.

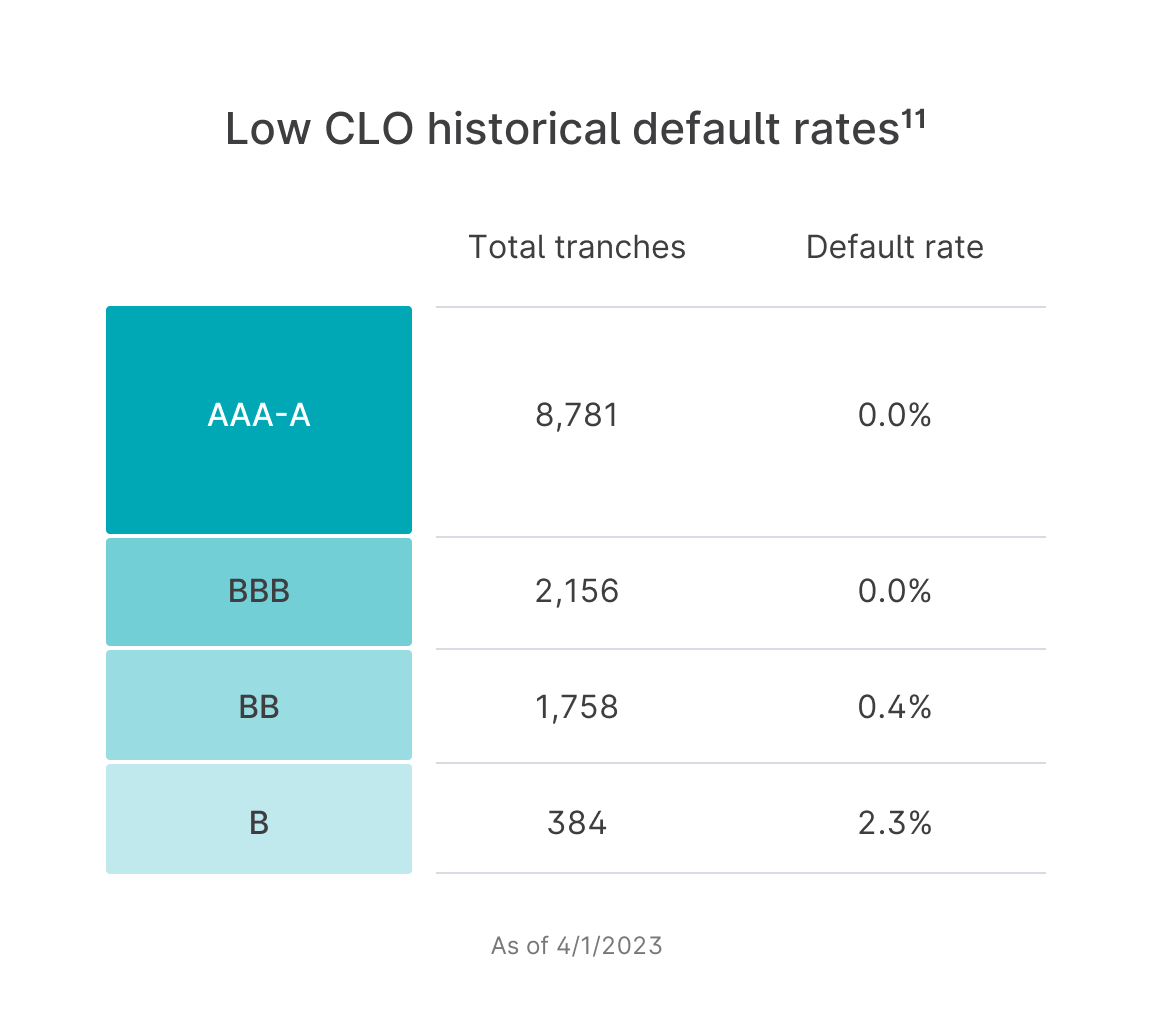

Near-zero default rates

Historically, the CLO structure has proven to be extremely resilient through multiple market cycles.

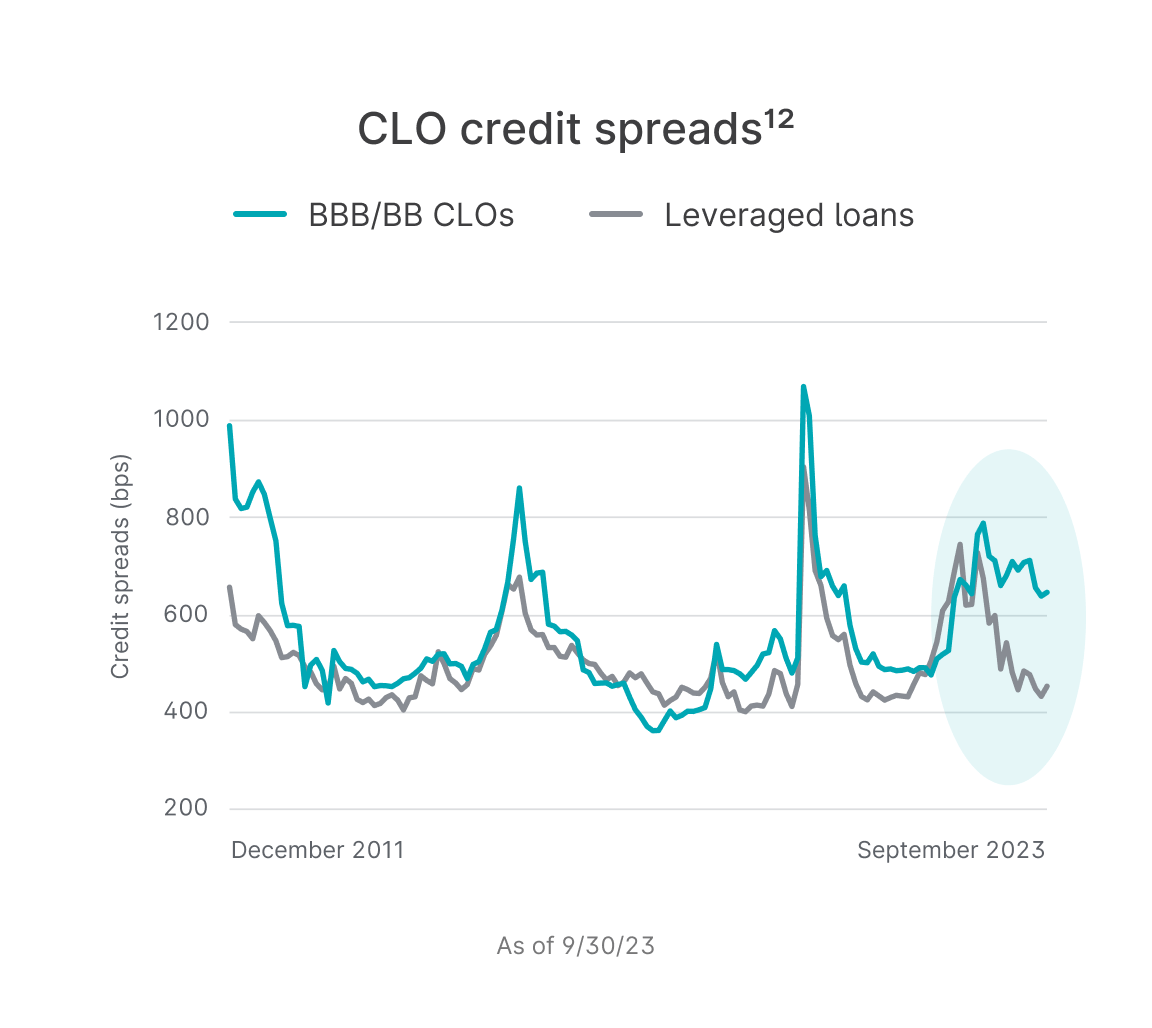

Uniquely wide credit spreads

Wider spreads, a measure of credit risk, allow CLOs to be purchased at a potential discount. As spreads normalize, CLO resale prices are expected to rise.

Access diversified Funds of CLOs

Yieldvilla offers Funds of BBB and BB CLO tranches.

Diversified collateral

Each CLO is collateralized by 200+ senior secured loans issued by companies with typically $100M+ of EBITDA.

Ultra-low default rates

The BBB and BB tranches have average default rates of 0% and 0.4%, respectively.¹¹

Top-tier managers

The Funds will only purchase CLOs structured by prominent asset managers such as Blackstone and Goldman Sachs.

The first private market platform to offer CLOs

We have partnered with Prytania Asset Management as the sub-advisor for our Diversified CLO Funds.

$1T+

CLO market globally¹³$2.2B+

Prytania AUM20 yrs

Prytania years in businessDive deeper

How CLOs work

These slides explore the fundamentals of CLOs and how the unique tranche structure helps protect investors.

The opportunity in CLOs with Prytania Asset Management

Mark Hale, CEO and CIO of Prytania, joined Yieldvilla to discuss the benefits of CLOs for investors.

CLOs vs. other investment products

See how CLOs compare to various fixed income and structured products.